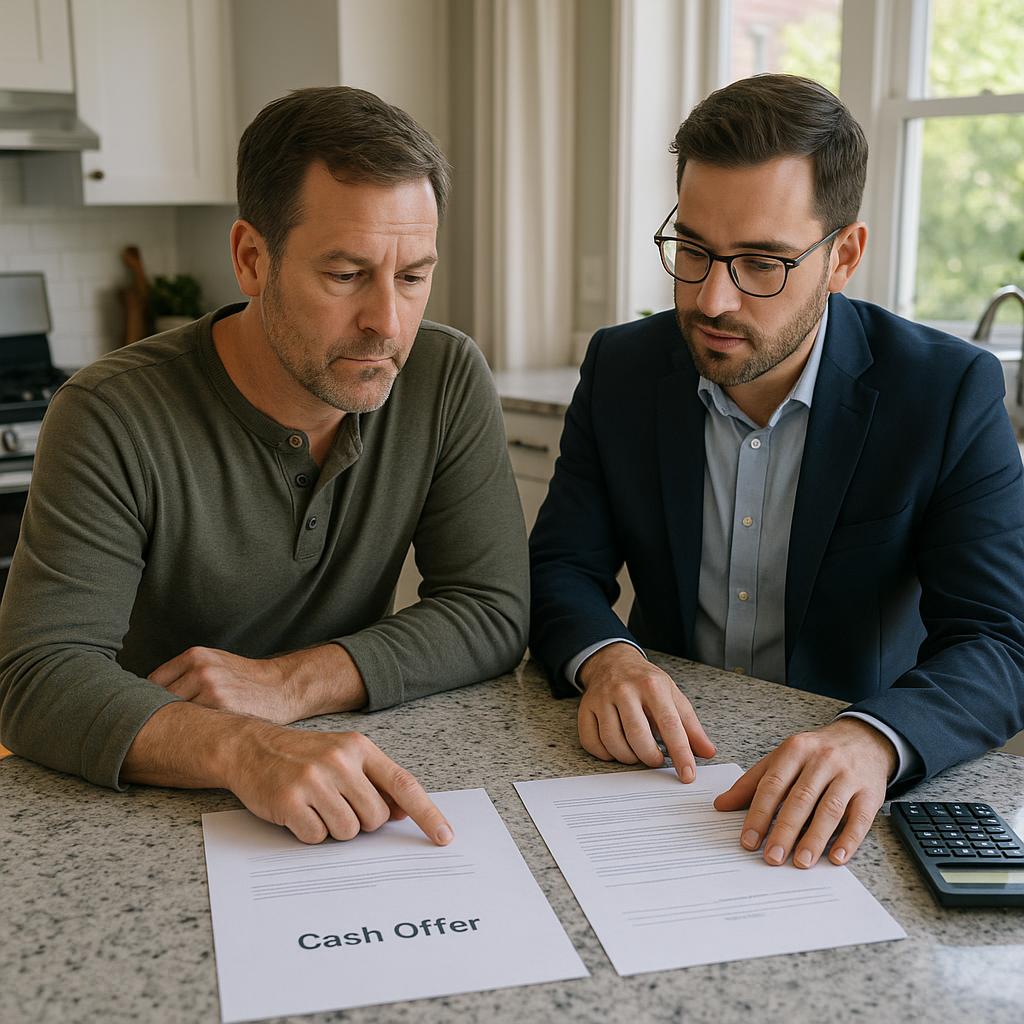

Should I accept a cash offer on my Grand Rapids home?

If you’re selling your home in Grand Rapids and you’ve just received a cash offer, you might be wondering if it’s the right move to accept it. Cash offers can seem tempting—there’s the promise of fewer hurdles and a faster close—but as a seller, it’s important to weigh all the pros, cons, and market factors before making your decision.

Many Grand Rapids sellers are surprised when a cash offer lands on the table, especially if they expected most buyers would need a mortgage. Understanding what accepting a cash offer actually means for your bottom line, your timeline, and your peace of mind is crucial. Let’s break down what you should consider from a seller’s perspective.

Quick Answer

Accepting a cash offer on your Grand Rapids home can reduce risk and speed up your sale, but it’s not always the best choice if the price or terms aren’t right. Cash buyers often expect a discount or fewer contingencies, so you’ll want to compare their offer carefully against financed offers, especially if your listing is generating strong interest.

There’s no one-size-fits-all answer—your decision should be based on your goals, the market’s response to your home, and how the offer terms align with your needs. If you’re dealing with this, I’m happy to walk through it with you.

1. Pricing: Is the Cash Offer Competitive?

The first thing sellers should evaluate is whether the cash offer reflects the true market value of their Grand Rapids home. Cash buyers often expect a lower price in exchange for a quick, hassle-free close. In a strong market where homes are getting multiple financed offers, cash offers may come in lower than the highest offer on the table. However, a lower cash offer might still be attractive if it eliminates appraisal or loan risk.

Jason’s take: “I always advise Grand Rapids sellers to weigh the cash offer not just against the list price, but against what the market is actually delivering. If showings are strong and offers are competitive, don’t rush to accept a cash offer that’s thousands below your other options.”

If your listing isn’t generating much activity, a cash offer—even at a modest discount—might be worth serious consideration, especially if your priority is certainty and speed.

2. Positioning: What Risks Does a Cash Offer Remove?

Cash offers typically remove two major risks for sellers: appraisal risk and lender risk. With a traditional financed offer, your sale can fall apart if the appraisal comes in low or if the buyer’s loan is denied at the last minute. According to the National Association of Realtors, appraisal and financing issues are among the top reasons sales fail to close on time.

Jason’s take: “When a seller absolutely needs to move on a certain date or can’t afford the deal to fall through, a cash offer removes a huge layer of uncertainty. That peace of mind is sometimes worth more than an extra few thousand dollars.”

If your timeline is tight, or you’ve had a previous deal fall through due to financing, the reduced risk of a cash offer can be extremely valuable.

3. Timing: How Fast Do You Need to Close?

Cash offers usually close faster—often in as little as 10-15 days compared to 30-45 days for financed deals, according to Consumer Financial Protection Bureau guidance. If you need to relocate for a job, buy another home, or simply want to avoid carrying two mortgages, a cash offer’s speed can be a game-changer.

But don’t let the promise of a quick close blind you to other important factors. If you’re not ready to move immediately, or if you need post-closing occupancy, make sure the cash offer’s timeline actually works for you. Sometimes, a financed buyer willing to work with your schedule is the better fit.

4. Negotiation: What Terms Can You Leverage?

Just because a buyer is paying cash doesn’t mean you can’t negotiate. Sellers in Grand Rapids can often get better terms—such as selling “as-is,” minimizing inspection requests, or securing flexible possession—when working with a cash buyer. Some cash buyers are also open to short-term rent-backs if you need time after closing.

Jason’s take: “I’ve helped Grand Rapids sellers negotiate solid as-is terms with cash buyers, saving them thousands in repairs and post-inspection hassles. Don’t be afraid to ask for what you need in the deal.”

Be sure to review all contingencies, not just the price. A strong cash offer should minimize hoops for you as the seller, but you still want to ensure you’re protected if something unexpected comes up before closing.

Real Seller Case Study: Grand Rapids Cash Offer Decision

Last fall, a Grand Rapids homeowner I worked with received a cash offer two days after listing their home. The offer was $12,000 below asking, but included no appraisal and minimal inspection. At the same time, we received a full-price financed offer with standard contingencies. The seller’s priority was certainty and a fast close, but they didn’t want to leave money on the table. We countered the cash buyer to bridge some of the price gap, and ultimately negotiated a sale $6,000 above their initial cash offer, closing in under three weeks. The seller avoided appraisal worries and moved on schedule for a job relocation.

Grand Rapids Market Insight

In Grand Rapids, I’ve noticed that cash offers are most common on homes that are move-in ready or need only minor updates. Sellers with unique properties or those needing repairs may see more cash interest, since these buyers are often investors or want to avoid lengthy loan approval processes. Still, the strongest listings with high demand often attract multiple offers—including cash—but sellers should always compare terms, not just price.

Frequently Asked Questions About Selling in Grand Rapids

- Do cash offers usually come in lower than financed offers?

Yes, cash offers in Grand Rapids often come in below list price, but the trade-off is faster, lower-risk closing. Always compare the full offer package. - Can I still negotiate inspection terms with a cash buyer?

Absolutely. Many cash buyers are open to limited or as-is inspections, but you can and should negotiate the details that matter to you. - How quickly can a cash sale close in Grand Rapids?

Most cash sales close in 10-21 days, depending on title work and how quickly both parties can prepare for closing. - Is accepting a cash offer safer than a financed offer?

Cash offers remove appraisal and financing risk, making them less likely to fall through. However, always verify proof of funds before accepting.

Related Resources

- Should I Fix Things Before Selling in Grand Rapids?

- What Happens If My Grand Rapids Home Appraises Low?

- When Should I List My Grand Rapids Home?

About the Author

Jason Pohlonski

is a Michigan licensed real estate salesperson with Keller Williams Grand Rapids East. He helps buyers and sellers throughout Grand Rapids, East Grand Rapids, Forest Hills, Ada, Byron Center, Jenison, Cascade, and surrounding West Michigan communities.

Jason began his real estate career in Chicago in 2004, later expanding his experience in Ann Arbor from 2014 to 2019, and has been serving clients in the Grand Rapids area since 2019.

With over 20 years of combined real estate experience across multiple markets, Jason focuses on helping clients make clear real estate decisions involving pricing, offer terms, inspections, appraisals, relocation timing, and buy-sell planning.

Industry Recognition

Jason is recognized by platforms and industry organizations including Zillow, Grand Rapids Magazine Real Estate All-Stars, and Real Producers for his work serving West Michigan buyers and sellers.

Jason also supports One More Moment, a nonprofit that grants wishes to late-stage cancer patients, by donating $100 for every successful closing.

Professional Disclosure

Jason Pohlonski

Michigan Licensed Real Estate Salesperson

License Verification: Verify Michigan License #6501386166

Brokerage: Keller Williams Grand Rapids East

Brokerage Office: 630 Kenmoor Ave SE, Suite 101, Grand Rapids, MI 49546

📱 Call or text: 616-916-9770

📅 Schedule consultation:

https://calendly.com/pohlonskirealestate/30min

📧 Email: jpohlonski@kw.com

This article reflects real client experiences and market conditions in Grand Rapids and surrounding communities at the time of publication. Real estate outcomes can vary depending on market conditions, property characteristics, buyer demand, financing terms, inspection results, appraisal results, and lender requirements.

This article is for general informational purposes only and is not legal, tax, financial, insurance, engineering, inspection, or floodplain determination advice. Buyers and sellers should consult qualified professionals before making decisions involving financing, insurance, inspections, taxes, legal issues, or property risk.